The Great Acceleration: Technological Convergence

Source: ARK Invest Big Ideas 2026

Every January, ARK Invest drops Big Ideas.

That's a 100+ page report where they basically say "here's what's going to happen, and you're not ready." It's like a crystal ball, except the crystal ball has a portfolio and occasionally gets things very wrong.

I read it because I can't help myself. Then I thought, what if I actually tried to understand it instead of just nodding along and tweeting the cool-sounding parts? So here we are. Thirteen parts, zero pretense of being an expert. I explain what ARK says with my own understanding, poke holes where I see them, and share what I'm actually thinking. If I'm wrong, which happens, at least we'll all learn something.

Big Ideas 2026, Part 1: Five Technologies Are Converging at Once

ARK Invest thinks the global economy will grow at 7.3% annually by 2030. The IMF thinks 3.1%. That's not a rounding error. That's two completely different theories of how reality works, and one of them is going to look very silly in a few years.

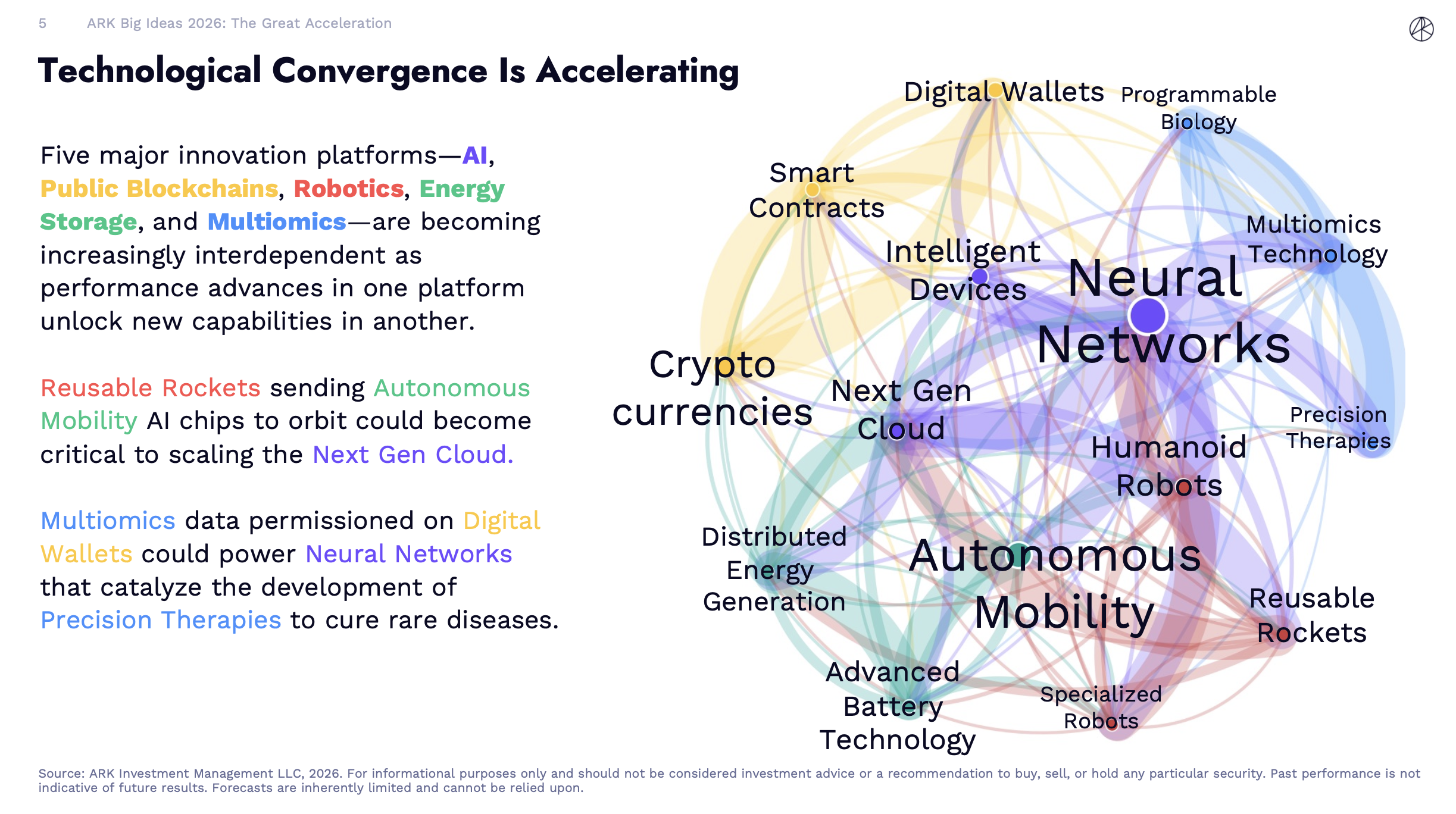

The Big Picture

ARK's overarching thesis for 2026 is what they call "The Great Acceleration": five major innovation platforms converging simultaneously, for the first time in history. The five platforms:

- Artificial Intelligence — the brain

- Public Blockchains — the financial rails

- Robotics — the hands

- Energy Storage — the power

- Multiomics — the code of life (genomics, proteomics, and other biological data layers, now supercharged by AI)

ARK tracks this with an internal metric called "Convergence Network Strength," measuring how much these technologies are catalyzing each other. That metric grew 35% in 2025 alone. (Worth flagging: this is ARK's own proprietary metric, not independently verified. Treat it as directional, not precise. ARK is not exactly a neutral party here.)

Here's why convergence matters more than any single platform improving. One technology getting better is a straight line. When technologies feed each other, you get feedback loops, which compound. AI improves robotics. Robotics generates physical-world training data that improves AI further. Cheaper rocket launches enable global satellite connectivity. That connectivity lets AI agents operate anywhere. Operating AI agents anywhere creates demand for programmable money (stablecoins) so the agents can actually do things without a human countersigning every transaction. Each platform makes every other platform worth more.

The historical parallel ARK reaches for is the 1890s through 1920s: electricity, internal combustion engines, telephones, and assembly-line manufacturing all arriving at roughly the same time, each amplifying the others. Standard economic models projected the future by extrapolating the past. They got it badly wrong. ARK's argument: the IMF's 3.1% forecast is making the exact same mistake right now.

By the Numbers

~8% of GDP. Where ARK projects AI software investment is heading by 2030. For context: railroads, the defining infrastructure project of 19th-century America, peaked at roughly 5% of GDP. We have never seen a single technology absorb this share of the economy this fast.

~10%+ of GDP. Total projected technology investment once you layer in AI data centers (terrestrial and space-based) and robotaxis on top of AI software. "Unprecedented" is an overused word but it applies here.

$117 trillion. ARK's projected economic surplus unlocked by AI by 2030, cumulative over the decade. Here's the catch: software vendors only capture about $13 trillion of that (roughly 10%). The remaining $104 trillion flows to businesses as higher profits, consumers as lower prices, or workers as shorter hours with maintained pay. (I'd really like to believe that last part. I'm just not convinced that $104 trillion in productivity gains shows up in anyone's paycheck equally.)

To put the 8% in perspective: software investment from the 1990s through the 2020s peaked at about 2.5% of GDP. AI investment is projected at more than three times that, arriving faster. That's the kind of number that sounds made up until you look at the data centers being built right now.

What's Actually Happening

The feedback loops are real and already running. Here's one concrete example using a single supply chain transaction.

A company wants to source components. An AI agent analyzes suppliers globally and identifies the best option in Southeast Asia. It needs to pay a deposit. It does so instantly via stablecoin on a public blockchain. No wire transfer, no human approval, no three-day bank processing. The components are assembled partly by humanoid robots in a factory powered by co-located solar and batteries, not the grid. The finished product ships to a satellite-connected warehouse in a region where Starlink provides the only connectivity. That warehouse is coordinated by AI logistics software. Every step generated data that improved the AI models involved.

None of these five platform pieces existed meaningfully 10 years ago. All five are functional today. That's the thing that should make you stop and actually think.

ARK notes that 2025 was the year robotics shifted from being a recipient of innovation (benefiting from AI, better batteries, cheaper sensors) to a catalyst that accelerates everything else: generating physical-world training data, creating energy demand, requiring blockchain coordination to operate in fleets. The 35% jump in convergence strength reflects platforms that are no longer just developing in parallel. They're feeding each other now.

Get the next deep dive in your inbox

The Bull and Bear Case

Bull case: If the convergence is real and the feedback loops tighten as projected, ARK's GDP forecasts may actually be conservative. The railroad investment wave at 5% of GDP underpinned a century of US economic dominance. A wave at 8-10% of GDP, compressing decades of progress into years, could produce returns that make even ARK's projections look modest. Companies sitting at the intersection of multiple platforms (Tesla spanning AI, robotics, energy storage, and autonomous vehicles is the obvious example) could see asymmetric upside. This is the part of the pitch that makes it genuinely hard to dismiss.

Bear case: The most important risk ARK mostly glosses over is the fiber optic parallel. In the late 1990s, telecom companies invested massively in internet infrastructure. That fiber is still in the ground and still powers much of the internet today. The technology worked. Many builders went bankrupt anyway, because returns didn't materialize fast enough to service their debt. Value accrued to the users of the infrastructure (Amazon, Google) not the builders. Worldcom and Global Crossing collapsed despite building genuinely useful things.

ARK's own model hints at this tension. Of the $117 trillion in economic surplus, software vendors capture $13 trillion. The other $104 trillion flows elsewhere. High CapEx as a percentage of GDP measures conviction. It does not guarantee returns. That distinction matters enormously if you're thinking about what to actually own.

There's also the timeline problem. Technology transitions of this scale have historically taken longer than optimists project. ARK's 7.3% GDP growth rate assumes best-case adoption curves across all five platforms simultaneously. Regulatory friction, geopolitical risk (chip export controls are already a real variable, not a theoretical one), energy bottlenecks, and the plain difficulty of deploying complex technology at scale could extend the timeline significantly. Cathie Wood has been early before.

Now the part most Western forecasts quietly skip: China's position in this convergence is not peripheral. Three of the five platforms, robotics, energy storage, and AI hardware supply chains, run through Chinese manufacturing in ways that are genuinely hard to route around. Beijing has explicitly targeted humanoid robotics and solid-state batteries as national strategic priorities, with subsidy programs already running. Chinese EV and battery companies (BYD, CATL, and others) are already operating at the cost curves ARK projects as 2028-era milestones. For readers watching from both sides of that equation: the convergence story looks meaningfully different depending on which side of the export control line you're on, and which platforms you think are actually most contested.

So What: What This Means for You

If you're an investor: The convergence thesis is ARK's frame for their entire portfolio: AI infrastructure, robotics, Bitcoin, energy, genomics. The key question to stress-test is where the $117 trillion actually lands. Software vendors capture $13 trillion. Are you betting on the builders or the users? The returns may end up in very different places, and history has a strong prior that the users win. Build your position around that prior, not the excitement of the infrastructure buildout.

If you're in tech or thinking about your career: The 35% jump in convergence strength means cross-platform skills are becoming more valuable than deep single-platform expertise. Engineers who understand how AI, energy, and blockchain fit together, even at a high level, will be better positioned than those who only know one domain. The next decade rewards generalists who can bridge platforms. This isn't a warm fuzzy career tip, it's what happens structurally when five industries collapse into each other.

If you're just curious: We're living through the equivalent of the 1890s, when electricity and cars and telephones all showed up at once and nobody quite knew what to do with the combination. Most people understood that things would be different. Very few understood how the value would actually distribute. The question isn't whether these technologies will change everything. It's whether the builders or the users will capture the value. History has a pretty clear answer on that one.

This is Part 1 of a 13-part series breaking down ARK Invest's Big Ideas 2026 report.

Disclaimer: This is not investment advice. This article examines ARK Invest's publicly available research report and stress-tests its claims. Nothing here should be taken as a recommendation to buy or sell any asset.

Sources

- ARK Invest Big Ideas 2026: Primary source report covering the five-platform convergence thesis and all financial projections cited in this article

- The Late 1990s Telecom Bubble: Historical context on the $500B fiber optic overbuild, Worldcom and Global Crossing bankruptcies, and the builder-vs-user value distribution

- Cathie Wood's ARK Invest predicts AI, other tech's great acceleration: InvestmentNews coverage of the "Great Acceleration" thesis and convergence framework

- Making It Up in Volume: How the AI Infrastructure Boom Echoes the Telco Frenzy of the 90s: Analysis drawing direct parallels between current AI CapEx and the 1990s telecom infrastructure cycle

- Big tech spending on AI data centers vs the fiber optic buildout: IEEE ComSoc comparison of AI infrastructure spending to the dot-com era